Don’t Fear The Reaper, Blue Oyster Cult, 1983

In this issue:

Jackson Hole thoughts

Bonds leading the narrative

Long-term outlook

Short-term outlook

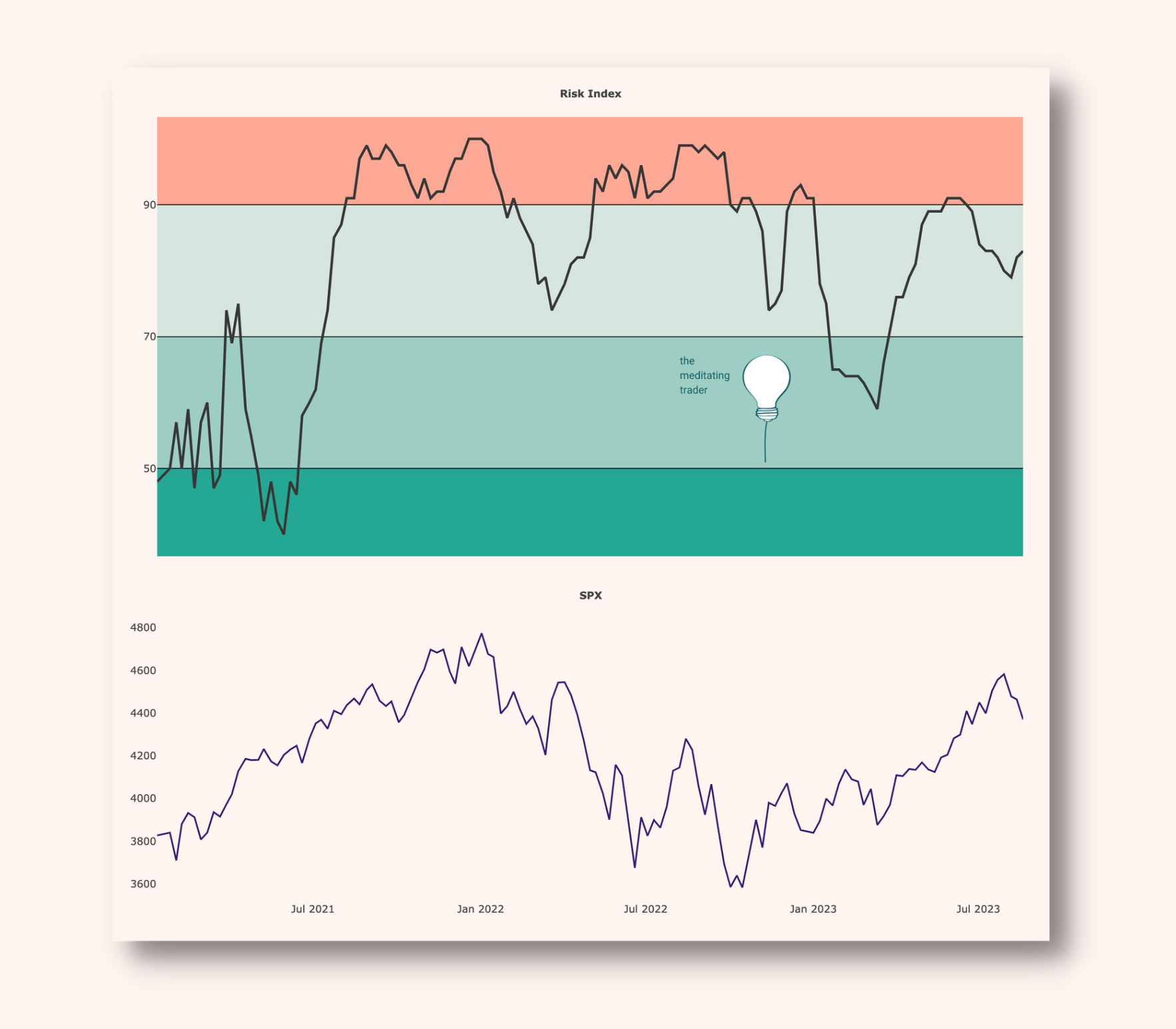

Risk Index

Under 50 = accumulate, over 70 = defensive, over 90 = distribute

The Risk Index is a combined read of the trends of 68 intermarket spreads and indicators, from credit spreads in the US to car sales in Spain.

The Risk Index called for weakness within the following 6 months back in June and it seems like we’re in the midst of that now. It would be great to see the Index move far lower and signal a buy in a few months. Currently, no-man’s land, but evidence points to more downside in the short-term.

Any key inputs?

Preliminary PMIs Wednesday

Jackson Hole Thurs through to the end of the week

Last year’s Jackson Hole was one of Powell’s most memorable moments, where he chose to shorten his speech compared to his allotted time and told the world, ‘be ready, inflation is our enemy and we don’t care what gets in the way.’ This resulted in a heavy drop in equities on the day and a continuation of the bear market with the S&P losing 16.5% over the next few months (notably into the lows that are still holding).

I don’t expect any such theatrics this year - they are not needed - but am watching to see if there is equity strength heading into Jackson Hole. That may set up a fade late this week. A strong bounce over a few days would also indicate that volatility has returned and we’re going to get some serious storms in risk assets in September.

Bonds

If this correction is a nasty one, it will be largely due to the ridiculous pricing of the mega-caps. They need to come back down to earth for anything constructive to happen longer-term (see the latest Trader Diary for more).

However, the mega-caps are the reason equities currently have the capacity for a major downdraft. The catalyst, at present, looks to be the action in various bond markets. This week's buzz-view: the inflation picture has ‘structurally changed’.

Knowing my own limitations as a human with minimal computing power (we like to call our computing power our brain and have a very inflated opinion of it), I try not to fortune tell on the inflation front.

However, it is notable that the narrative around inflation is not being driven by inflation! In the US, for instance, it has gone from around 9% YoY to 3% YoY. Most major economies are in MoM deflation. Let’s hope that doesn’t last too long. Nothing good ever came of long-term deflation.

So, if it is not inflation, what’s driving the inflation narrative? Bonds.

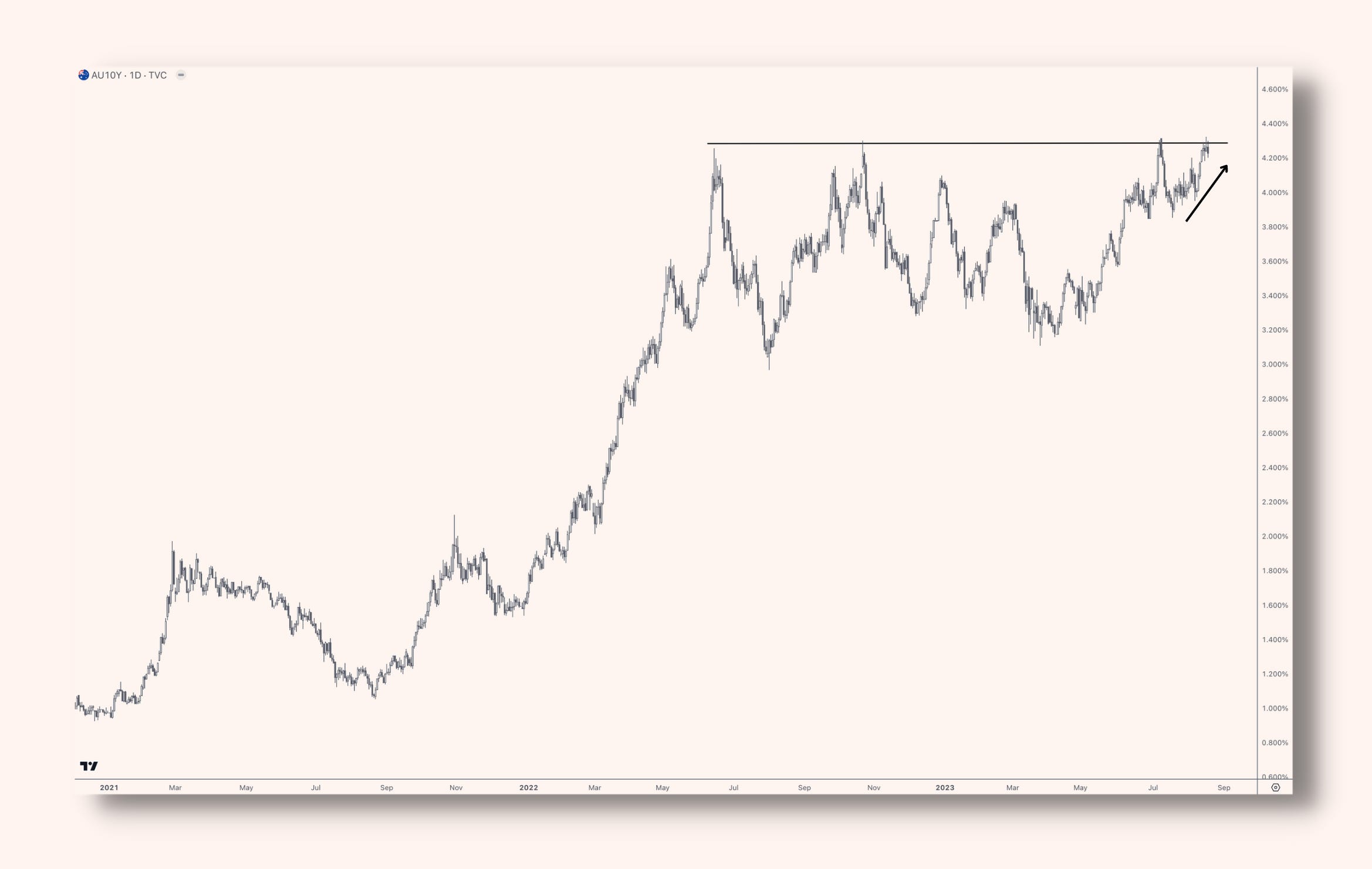

Let’s have a quick look at Aussie bond yields (mirrored in most developed countries).

Australian 10Y yields - look to be about to break higher. This, some may say, indicates a belief that yields will remain higher for longer due to inflation remaining higher for longer.

New Zealand yields have already broken higher

Interesting thing is that the 2 year yields have been moving down over the last few months.

Taken together, this seems to indicate a belief that although there may be a short-term dip in inflation, longer-term inflation will bounce back higher.

So, if the inflation narrative is being pulled along due to bond dynamics rather than inflation itself, the narrative starts to feel a bit off.

What greatly affects yield levels? Quantitative easing (QE).

One of the explicit aims of QE was to keep yields down. So, is it any surprise that yields have taken off like bats out of hell with QE currently replaced by quantitative tightening (QT)?

So, with an abundance of caution, as always, we can expect a possible turn of events over the coming 6 months:

yields break higher, ‘inflation forever’ narrative reaches a clamour while we see inflation itself continue to tick lower, confirming the narrative is likely to be wrong.

equities take a tumble partly due to the inflation narrative, and also as high yields = equities are increasingly unattractive. Risk-free US 10-year bonds at high yields instead? Yes, please.

this sets up a great buy in bonds (likely equities as well)

I like this view as the narrative (inflation forever) is increasingly becoming divergent from the data. I am most cautious about timing: this could be a view that plays out a year or more from now, after another jump in inflation in between or we could be watching it play out now.

When inflation spikes, it often does so more than once. Inflation spiking, at the heart of it, is an indication that monetary control policies have become of out sync. If we’re looking to trade against the prevailing narrative that is also currently backed up by the trend in yields, best to keep in mind that monetary policies may not steady the boat on the first try.

Zooming back in

Anyway, enough of the big picture. Shorter term, Friday could have instigated a little bounce into Jackson Hole (or perhaps a bit longer, into the start of September). However, there is no sign that the weakness has fully played out. This is likely the bounce that bulls buy thinking it is business as usual, and then they will become the sellers that drive the next swing lower.

Summed up by my 8,500 stock scan. Stocks within 3% of all time highs (middle, green line) never achieved the breakout we were looking for to confirm the strength in equities (S&P, top).

Conversely, stocks within 3% of all time lows (bottom, red line) reached very low levels earlier this year and look to have made a higher lower while equities have been moving up. This means more stocks have been weakening while the S&P has been moving higher. That’s not a nice divergence.

In short, there’s plenty of slack in individual stocks to drive this correction a lot lower in September.

Quote to Self

If there is more weakness in the coming month or so, that equals higher volatility. Both to the downside and the upside.

"Never let the fear of striking out keep you from playing the game."

~ Babe Ruth ~

A volatile trading regime after a period of relative calm tests discipline.

Discipline always erodes during the calm, and that erosion is not revealed until the storm. Then, gains of the year can be lost, fear appears, and trades that should have been taken are not. Problems compounding rather than your trade balance.

It’s time to check over your process and make sure every part is locked down so fear doesn’t get a look in at just the wrong moment.

Have a great week.