A Knock At The Door, Life Magazine, Walter Tittle, 1911

In this issue:

Cruisin’ for a bruisin’?

Realism with PMIs

RBOB divergence

Risk Index

Under 50 = accumulate, over 70 = defensive, over 90 = distribute

The Risk Index is a combined read of the trends of 68 intermarket spreads and indicators, from credit spreads in the US to car sales in Spain.

We’ve not had any extremes for some time - really since the Corona Crash. Extremes are outliers. I.e. we shouldn’t expect them. But we can plan for them, as noted below.

Any key inputs?

Sun: Caixin Manufacturing PMI

Mon: US Manufacturing PMI & a Powell speech

Tue: (early morning) RBA rate decision

Wed: (early morning) RBNZ rate decision

Fri: NFP

A narrative that seems very odd at present is that we are in a ‘soft or no landing’. As in, central banks managed to raise rates significantly, and we had very high comparable inflation, and that has done nothing to dampen economic activity.

When the Fed started raising, commentary rightly said that it would take some time to filter into the economy. The cumulative effect is only just seeping in. Let’s not be tricked by our poor grasp of time.

So, PMIs continue to be interesting. I saw a post today pointing out that they were showing ‘green shoots’. PMI charts are deceptive, as when they flatten out, it means very different things depending upon what level they flatten out. US PMIs (and many other global PMIs) are ‘flattening out’ below 50. Below 50 means contraction. So they are contracting at a slightly slower pace. On any other chart, the line would still be moving lower.

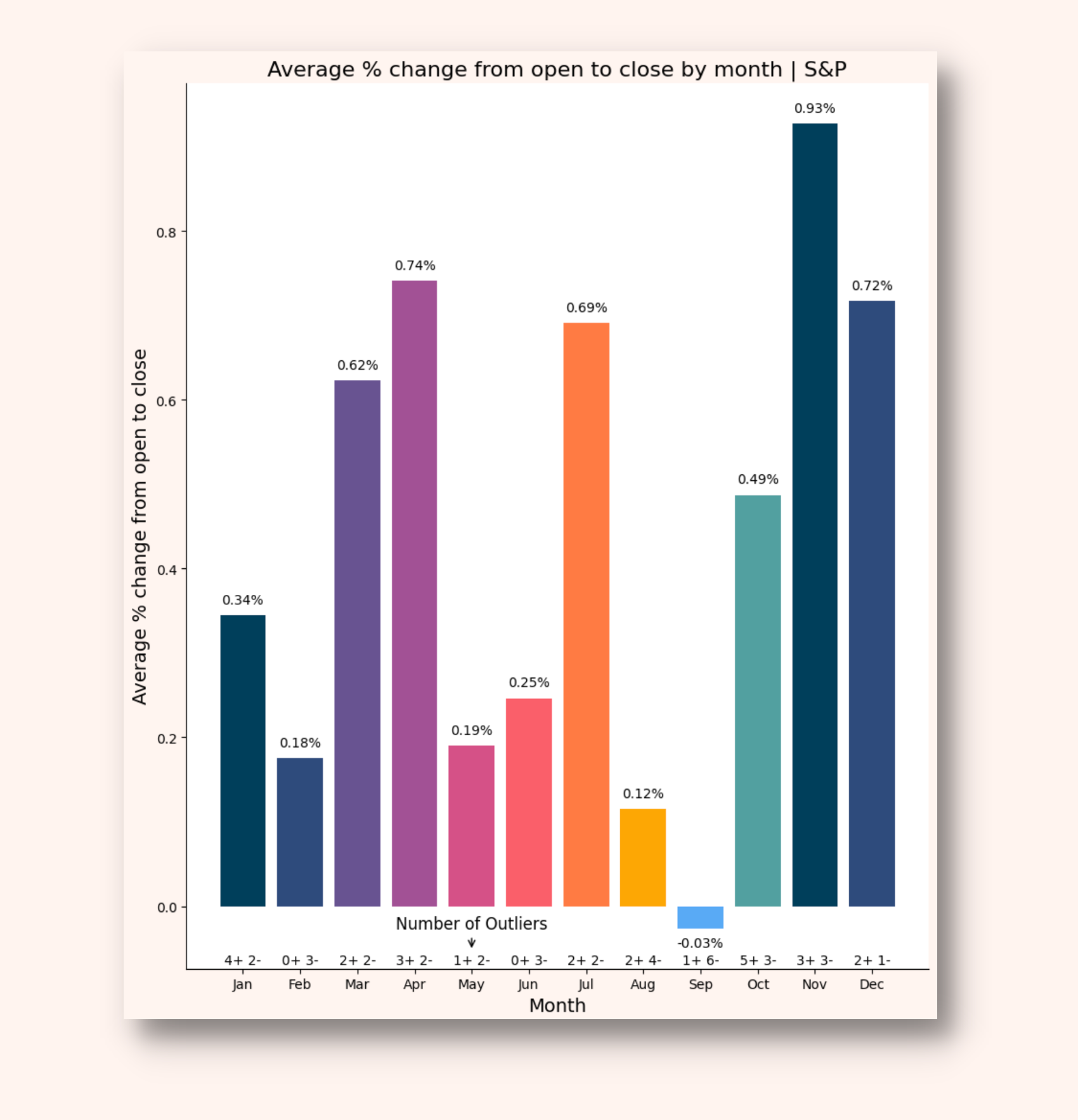

Seasonals: bullish…soon

August and September are the best time of the year to look for short trades in equities and 2023 has not disappointed, with some great setups from the end of July onwards.

These moves have largely played out, and my mantra to ‘never get short in Q4’ is kicking in….however, I’m still short Russell and S&P. It’s a tricky moment; these trades haven’t reached their targets.

October is certainly the time for a bounce.

Monthly % changes of the S&P, going back around 100 years (the %’s change depending on what years are kept in but the Q3 weakness and Q4 strength is pretty robust).

As noted in my last post, yes, October is seasonally positive and usually the start of the ramp into Christmas. However, it’s also the month with the most historic outliers. The most volatility. That’s interesting, considering where the Vix is:

VIX hasn’t been off the floor despite the equity weakness. Apparently ‘everyone’ is bearish. Odd that no-one is pricing in volatility.

Looking at weekly averages, the first few weeks of October aren’t as strong as seasonals would indicate - it just makes up for it by the end.

10 = October. Seems it often needs to go down before up.

Looking at some ‘oversold’ indicators, there’s still room for a downside flush. It would actually be pretty healthy.

S&P stocks v’s key MAs. 20 and 50 MA indicator certainly getting pretty extended - but room for a bit more downside if given a push.

Volume has been creeping up as well, a good sign that there’s a fight going on at this level.

Dow Jones here, because it often gives cleaner signals. Volume up, though no big spike yet like those we saw at the last two swing lows.

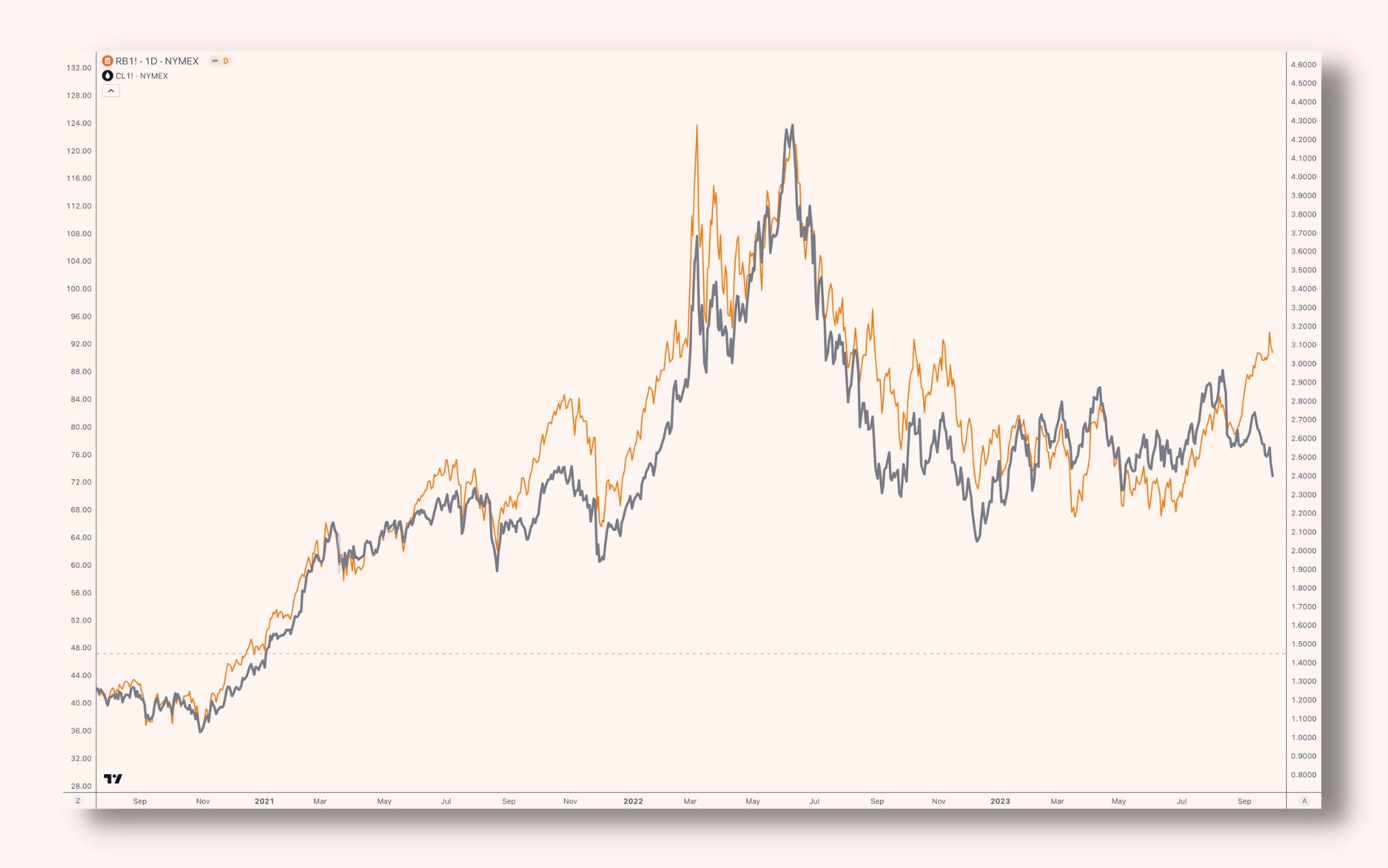

As an aside, oil ramped up into some clear resistance and setup a nice short. I’m in profit but unsure: momentum was certainly in the bulls favour. However, the spread between crude and RBOB is significant. It always comes back in, just a question of which way it will turn. Some quant analysis on whether one leads the other is in order this week.

Crude oil (black) and RBOB (orange). One of them lost the memo over the summer.

Quote to Self

So, overall, I’m up for taking the foot off the bear pedal until next year, but happy to hold onto shorts over the next two weeks to see if there is a flush to the downside.

October does like to surprise; stay frosty out there.

"Surprises are foolish things. The pleasure is not enhanced, and the inconvenience is often considerable."

~ Jane Austen ~

Have a great week.

Risk Index is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.