Fed up with the ECB?

Moonlit Harbour in Southern Italy (1833):

currently sitting in a museum in Norway

The ECB supposedly came to Italy (and the rest of Europe’s) rescue last week. Judging by some of the intermarket moves, players are undecided as to whether they will manage to pull it out the bag.

With the Fed this week, it’s time to see if the sun is setting on the European dream (doubt it, but it’s going to happen one day - no monetary union has ever lasted; our brains aren’t sophisticated enough to cope with them).

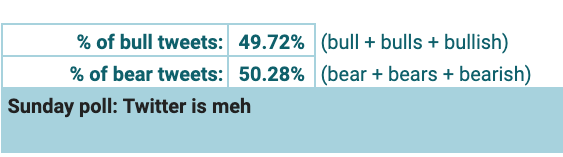

Sunday Twitter Poll

FinTwit is about flat this week. Last week it was bearish and it was a bull week; coming to expect it.

(Of the last 18,000 tweets containing SPX, $SPY or $ES, those including bull/bulls/bullish/bear/bears/bearish extracted, then % totals of each. Started April 2022; plan to track % of times Twitter is correct compared to the following weekly close. Tracking data will be added after the first 20 weeks.)

Roadmap

Wednesday - Fed interest rate decision. 75 bps priced in. They are going to have to go some way to surprise on the hawkish side.

Thursday - European CPI and US preliminary GDP.

Friday - European preliminary GDP & month end

A bunch of European PMI’s fell into contraction last week and the US was propped up by their manufacturing PMI, with services nose-diving. GDP’s to follow suit? - though likely the PMI’s won’t feed through until Q3.

Equities:

Markets had a soppy moment on Friday but didn’t like it and hung lower on the day. All in all, however, that’s a decent weekly close - the summer rally is holding on, for now.

A Bear has a poetic way of taking the rake from both sides, but that 3900 level now looks like a pretty good line in the sand if Friday’s sell-off drags price down there. Ball is in the Bull’s court.

FX:

A decent week for currencies v’s USD. Attention has been on the Euro due to parity but it has really been a USD story, with all other currencies falling heavily v’s USD this year as well.

Similar to equities, the closes last week points to some more USD weakness in the near term. If USD goes nowhere/ strengthens slightly by Wednesday and the Fed doesn’t surprise on the hawkish side, it could bring another leg down for USD in a heavier retracement.

EURUSD is allowed to punch another 3% higher and still be in a heavy downtrend:

Precious Metals:

The bounce at the end of last week got a few excited. Still waiting for that equity sell off to indicate the money supply has become too tight and the Fed has to pivot: then gold will be more than just a shiny thing.

Trades Update

This has moved to a free Thursday trades record, also available (most weeks) on Substack:

Risk Index

Under 50 = bullish, over 70 = bearish, over 90 = potential correction within 6 months

The Risk Index is a combined read of the trends of 68 intermarket spreads and indicators, from credit spreads to car sales in Spain.

Note that the current bear market was signalled 10 months ago (see reference down the bottom of this post at start of this year here) so the expectation is that the Risk Index will become increasingly bullish the longer this move down lasts.

1-year look-back:

If the market is working out a bottom, signs are that it will take some time to do so.

Themes to Watch

Keep reading with a 7-day free trial

Subscribe to Risk Index to keep reading this post and get 7 days of free access to the full post archives.